How to Build a Treasury Bill Ladder (Step-by-Step Guide)

Learn how to build a Treasury bill ladder to manage cash flow, improve flexibility, reduce reinvestment risk, and maintain regular access to your money.

A Treasury bill ladder is one of the simplest ways to manage cash while still keeping regular access to your money.

Instead of locking all your cash into a single Treasury bill with one maturity date, you spread it across multiple bills that mature at different times.

That creates a system where part of your money becomes available on a regular schedule.

For people trying to balance yield, flexibility, and predictable access to cash, that can be extremely useful.

A Treasury ladder does not try to predict where rates are going next.

It creates a structure that helps you stay flexible while putting cash to work.

Build your own Treasury ladder

Use the Treasurlytics ladder tool to test different amounts, maturity schedules, and cash-flow patterns before deciding how to structure your cash.

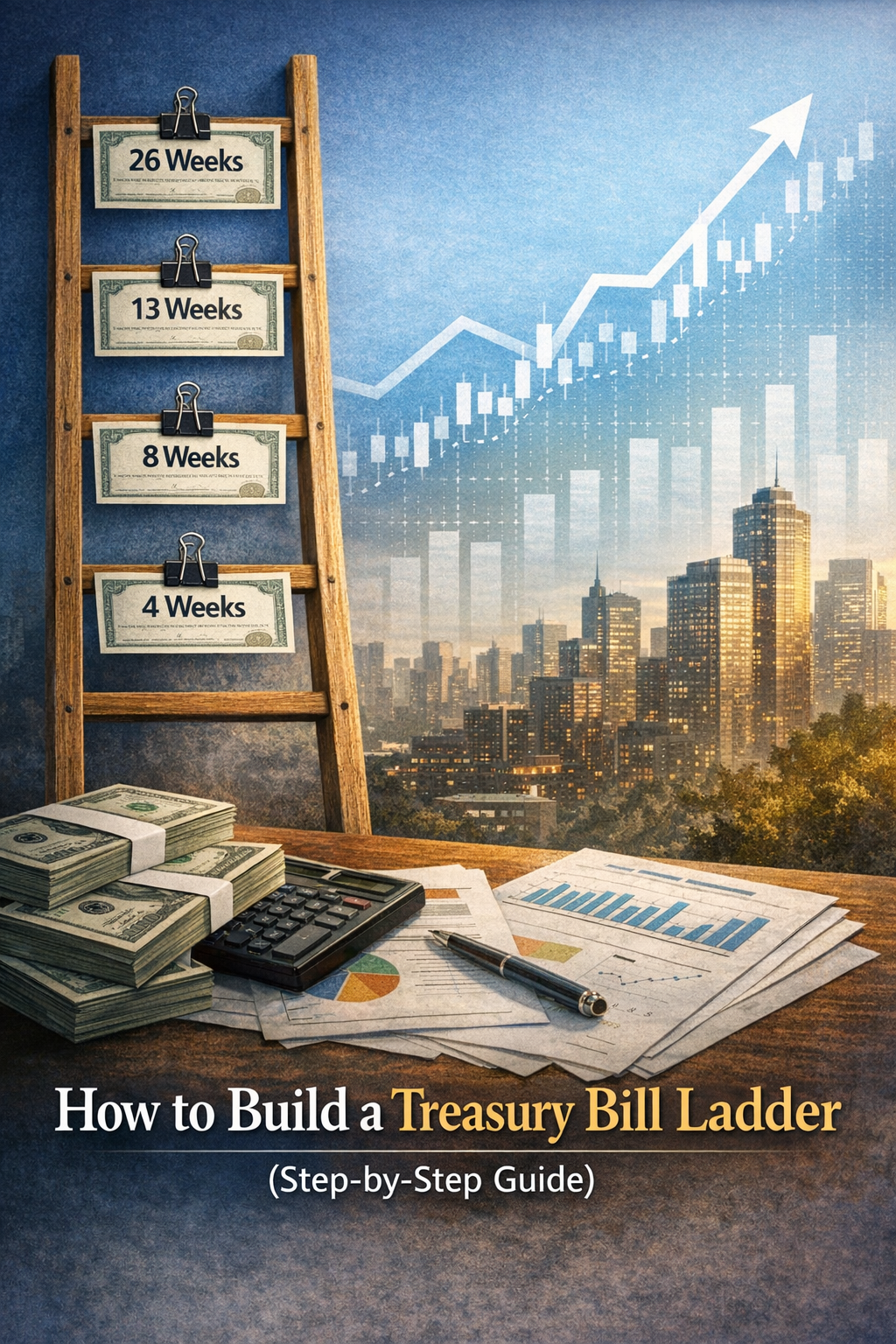

What Is a Treasury Bill Ladder?

A Treasury bill ladder is a strategy where you divide your cash across multiple Treasury bills with different maturity dates.

For example, instead of putting all your cash into one 13-week bill, you might buy:

- one 4-week bill

- one 8-week bill

- one 13-week bill

- one 26-week bill

As each bill matures, you can either:

- use the cash

- keep it in reserve

- reinvest it into a new bill

That is what creates the “ladder” effect.

Each maturity date acts like a rung, giving you scheduled access to part of your money over time.

Why Build a Treasury Ladder?

A ladder is useful because it solves a very common cash problem:

How do you earn something on idle money without locking all of it up at once?

A Treasury ladder helps you:

- maintain regular liquidity

- avoid making one all-or-nothing maturity decision

- reduce the need to guess the perfect time to invest

- adapt gradually as rates change

- keep part of your cash coming due on a schedule

Instead of treating cash as one lump sum, a ladder turns it into a system.

That makes it especially useful for people who want structure, not just yield.

Who a Treasury Ladder Is Good For

A Treasury ladder may make sense for people who:

- want to earn on short-term cash

- have money they do not need all at once

- want scheduled access to funds

- prefer a conservative cash strategy

- want an alternative to keeping too much cash in checking

- want to organize cash around expected expenses

Common examples include:

- emergency fund layers

- tax reserves

- business reserve cash

- home purchase funds with uncertain timing

- large upcoming expenses over the next few months

A ladder is especially useful when your money has a purpose, but the exact day you will need it is unclear.

Not sure which Treasury bill maturity to use?

Start by checking current rates, then use the calculator to estimate what individual T-bill positions could earn.

Who a Treasury Ladder May Not Be Best For

A ladder is not perfect for every situation.

It may be less useful if:

- you need all of your money available immediately

- your cash flow is highly unpredictable

- you are investing for long-term growth rather than short-term cash management

- you do not want to manage reinvestment decisions as bills mature

- you want the simplest possible account setup

If instant access matters more than yield, a savings account may still be the better home for at least part of your cash.

A ladder works best for money that is important, but not needed today.

Step 1: Decide How Much Cash to Allocate

Start by choosing how much cash you want to place into the ladder.

Example:

- $4,000 total

This should be money you want to keep relatively safe, but that you also want to earn something on.

Before building the ladder, ask:

- Is this emergency cash, reserve cash, or planned short-term cash?

- Will I need all of it at once, or only some of it?

- How often do I want access to part of it?

- How much should remain outside the ladder for immediate needs?

The answers will help determine your ladder design.

Step 2: Choose How Often You Want Access to Cash

Next, decide how frequently you want money becoming available.

Common choices include:

- every 4 weeks

- every 8 weeks

- every 13 weeks

- every month or quarter, depending on your structure

This is one of the most important ladder decisions.

The shorter the interval, the more often you regain access to cash.

The longer the interval, the simpler the ladder may be, but the less frequently money comes due.

Think of this step as choosing your liquidity rhythm.

Step 3: Choose the Maturity Structure

Now decide which Treasury bill maturities you want to use.

A simple beginner ladder might use:

- 4-week

- 8-week

- 13-week

- 26-week

This gives you staggered maturities across several time horizons.

A more conservative ladder might stay shorter.

A more yield-seeking ladder might tilt longer.

There is no single perfect setup.

The best structure depends on:

- how soon you may need the money

- how often you want access

- how much flexibility you want

- how comfortable you are reinvesting over time

Step 4: Split the Investment Across the Ladder

Once you choose your maturities, divide the money across those rungs.

Example with $4,000:

| Ladder Rung | Treasury Bill Maturity | Example Allocation | Purpose |

|---|---|---|---|

| Rung 1 | 4-week bill | $1,000 | Earliest access |

| Rung 2 | 8-week bill | $1,000 | Near-term access |

| Rung 3 | 13-week bill | $1,000 | Short-term cash |

| Rung 4 | 26-week bill | $1,000 | Longer short-term cash |

This is a simple equal-weight ladder.

You do not have to split everything evenly, but even splits are easy to manage and easy to understand.

Some investors choose uneven allocations if they expect to need more cash sooner than later.

Try this with your own numbers

Change the amount, maturities, and ladder structure to see how your cash could be spread across different Treasury bill maturities.

Step 5: Reinvest as Bills Mature

When the first bill matures, you have a decision:

- spend it if you need the cash

- hold it temporarily

- reinvest it into a new bill

This is where the ladder begins to work as a rolling system.

For example, if your 4-week bill matures and you do not need the money, you might reinvest it into a new 26-week bill.

Over time, the ladder becomes more stable because you continuously replace maturing bills with new ones.

That rolling process helps you stay invested while still maintaining regular maturity dates.

Example of a Simple Ladder

Suppose you start with this setup:

| Starting Position | Amount | Maturity |

|---|---|---|

| Treasury bill 1 | $1,000 | 4 weeks |

| Treasury bill 2 | $1,000 | 8 weeks |

| Treasury bill 3 | $1,000 | 13 weeks |

| Treasury bill 4 | $1,000 | 26 weeks |

What happens next?

| Time From Start | What Happens | Your Decision |

|---|---|---|

| 4 weeks | First bill matures | Use cash, hold cash, or reinvest |

| 8 weeks | Second bill matures | Use cash, hold cash, or reinvest |

| 13 weeks | Third bill matures | Use cash, hold cash, or reinvest |

| 26 weeks | Fourth bill matures | Use cash, hold cash, or reinvest |

If you keep reinvesting maturing cash into new bills, your money keeps working while still becoming available in stages.

That is the core benefit of the ladder:

you are never waiting for one single maturity date for all your money.

Monthly vs Quarterly Ladder Thinking

Not every ladder needs to look the same.

A shorter-access ladder

This works better for people who want cash available more frequently.

Example use cases:

- emergency reserves

- uncertain business expenses

- near-term household spending

A wider-spacing ladder

This works better for people who are comfortable with less frequent access in exchange for a simpler structure.

Example use cases:

- medium-term reserve cash

- planned future expenses

- funds that are unlikely to be needed immediately

The right ladder depends less on theory and more on how your cash actually behaves in real life.

Advantages of a Treasury Ladder

A Treasury ladder can offer several advantages.

Regular access to cash

Instead of locking everything into one maturity date, part of your money becomes available on a schedule.

Reduced timing risk

You avoid putting all your cash into the market at one single moment.

Better rate averaging

Because you reinvest over time, your ladder naturally spreads out rate exposure.

More flexibility

You can decide at each maturity whether to reinvest or use the cash elsewhere.

Stronger cash discipline

A ladder creates structure, which can help you manage cash more intentionally.

Risks and Trade-Offs to Watch

A Treasury ladder is conservative, but it is not magic.

There are still trade-offs.

You still need cash planning

A ladder helps with structure, but it does not replace understanding your actual cash needs.

Reinvestment risk

If yields fall, the new bills you buy may offer lower returns than the old ones.

Opportunity cost

If rates rise after you lock in some bills, newer opportunities may look better.

Early sale risk

If you need money before maturity and have to sell early, price risk can matter.

Administrative effort

A ladder is simple, but it still requires periodic decisions and maintenance.

These are manageable issues, but they are worth understanding before you start.

Common Mistakes to Avoid

Putting all cash in one maturity

That defeats the purpose of the ladder.

Making the ladder too complicated

A simple structure is usually better than an over-engineered one.

Ignoring your actual cash timeline

Do not build a ladder based only on yield if your money may be needed sooner.

Reinvesting automatically without thinking

Reinvestment is powerful, but each maturity is also a chance to reassess your needs.

Using a ladder for money that needs instant access

Some cash should remain outside the ladder if you may need it immediately.

Ladder Mindset: Structure Over Prediction

The real strength of a ladder is not that it maximizes yield in every scenario.

It is that it reduces the pressure to be right about the future.

Instead of trying to guess where interest rates are going next, you:

- reinvest steadily

- adapt gradually

- maintain flexibility

- keep part of your money available over time

That is why a ladder is often better understood as a cash management framework rather than a return-chasing strategy.

How a Treasury Ladder Compares With a Savings Account

A savings account and a Treasury ladder can both have a role in a cash strategy.

| Feature | Treasury Ladder | High-Yield Savings Account |

|---|---|---|

| Best use | Scheduled cash access | Immediate cash access |

| Liquidity | Available as bills mature | Usually immediate |

| Structure | Fixed maturity schedule | Open-ended |

| Rate behavior | Rates locked per bill at purchase | Rate can change anytime |

| Maintenance | Requires reinvestment decisions | Usually simple |

| Best for | Planned cash and reserve layers | Emergency cash and daily liquidity |

A savings account is usually better for:

- instant-access cash

- daily liquidity

- money you may need unexpectedly

A Treasury ladder is usually better for:

- structured short-term reserves

- planned liquidity

- cash you want to put to work without locking all of it up at once

For many people, the best answer is not one or the other.

It is a combination.

Immediate cash can stay in savings, while a ladder handles the portion of cash that can be scheduled more deliberately.

👉 Compare options here:

Compare T-Bills vs Savings

Build a Ladder With Real Numbers

Before building a ladder, it helps to see how the structure affects maturity timing and cash flow.

Use the interactive ladder tool

Test different ladder sizes, maturities, and schedules before deciding how to organize your cash.

You may also want to estimate what individual Treasury bill positions could earn:

And if you want a stronger foundation first:

Frequently Asked Questions

What is the point of a Treasury bill ladder?

A ladder helps stagger maturities so part of your cash becomes available regularly instead of all at once.

It is useful when you want structure, yield potential, and scheduled liquidity.

Is a Treasury ladder good for an emergency fund?

It can be useful for part of an emergency fund, especially money beyond the portion you want instantly accessible.

Many people keep immediate emergency cash in savings and use a ladder only for the reserve cash they are less likely to need right away.

How many rungs should a Treasury ladder have?

There is no fixed rule.

A simple ladder often starts with a few maturity points that match your desired access schedule.

For example, a beginner ladder may use 4-week, 8-week, 13-week, and 26-week bills.

What happens when one Treasury bill matures?

You can spend the cash, keep it available, or reinvest it into a new bill.

That maturity decision is what makes a ladder flexible.

Is a ladder better than buying one Treasury bill?

It depends on your goal.

A single bill is simpler, but a ladder usually offers better flexibility and more regular access to cash.

Do I need to put all my cash into a Treasury ladder?

No.

A ladder is usually best for the portion of cash that does not need immediate access.

Money you may need at any moment may be better kept in a savings or checking account.

Can Treasury bill ladders lose money?

If you hold individual Treasury bills to maturity, the repayment structure is highly predictable.

However, if you sell before maturity, market prices can matter.

There are also trade-offs like inflation risk, reinvestment risk, and opportunity cost.

Next Step

Choose the next step based on what you want to do next.

If you want to build a ladder now

Use the ladder tool to test maturities, allocations, and cash-flow timing.

If you want to check current Treasury rates first

Start with the live rates page before choosing maturities.

If you want to estimate one T-Bill position

Use the calculator to estimate a single Treasury bill’s potential return.

If you want to compare a ladder with savings

Compare Treasury bills against high-yield savings accounts as cash-management options.

If you want to understand T-Bills first

Learn the basics of how Treasury bills work.

Final Thought

A Treasury bill ladder turns a static pile of cash into a dynamic system.

It gives structure to your money and helps liquidity and yield work together instead of competing.

That is why laddering is useful.

It does not require perfect market timing.

It requires clarity about your cash needs and a willingness to build a system that matches them.

For people managing short-term cash carefully, a Treasury ladder can be one of the most practical and disciplined tools available.

The key is not to chase the highest possible yield.

The key is to match your cash with the right maturity schedule.