What Is a Treasury Bill (T-Bill)? How It Works, Why Investors Use It, and When It Makes Sense

Learn what a Treasury bill is, how T-bills work, how investors earn money from them, their risks, tax treatment, and when they make sense for cash management.

When people hear the word investing, they usually think of stocks, volatility, and the possibility of losing money.

But not every investment is designed for growth.

Some are designed for capital preservation, predictability, and short-term cash management.

One of the clearest examples is the Treasury bill, often called a T-bill.

If you want a simple way to earn a return on cash without taking the kind of risk that comes with stocks or lower-quality bonds, understanding Treasury bills is a good place to start.

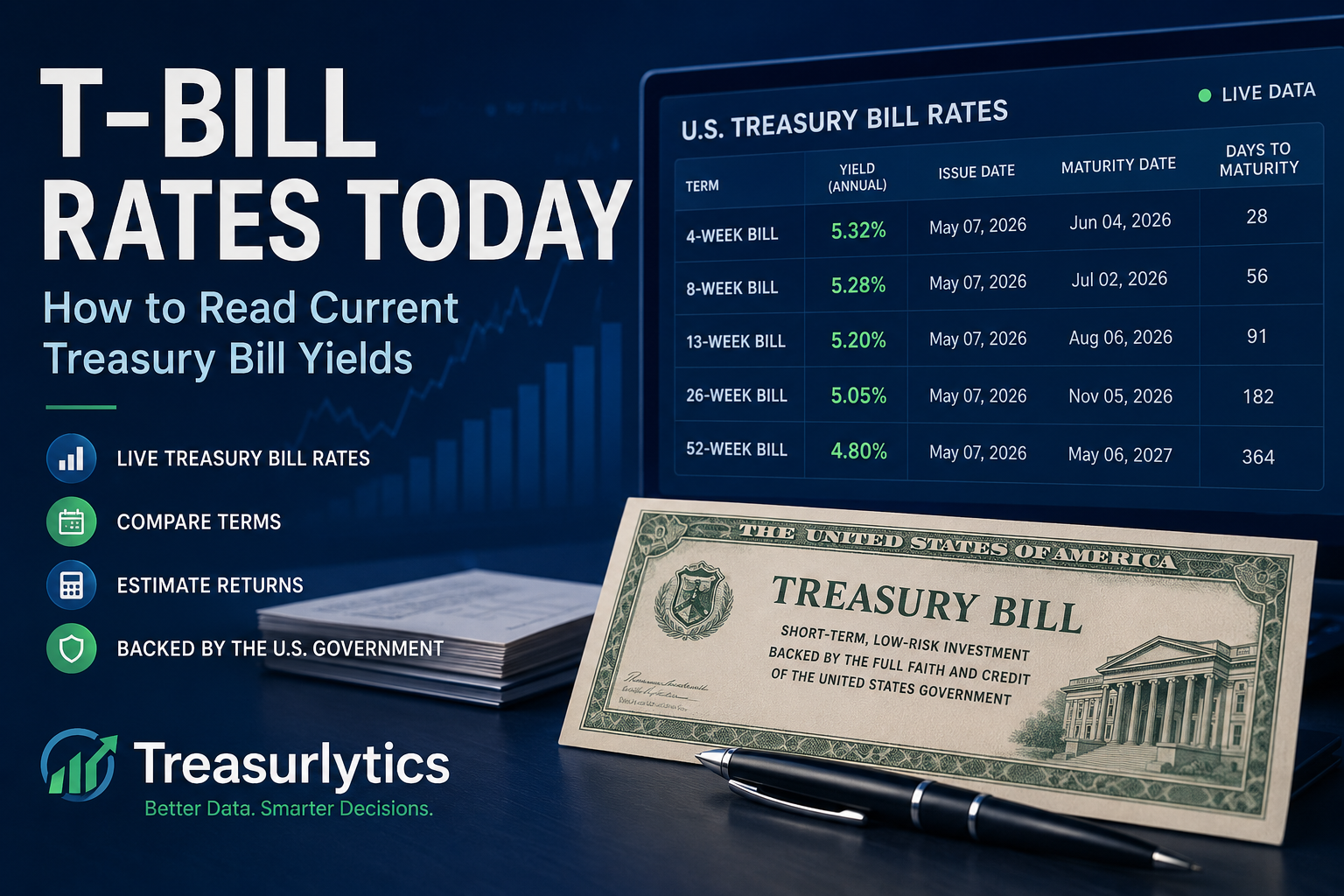

Want to see where T-Bill rates are today?

Before deciding whether a Treasury bill makes sense, start by checking current Treasury yields and comparing them with other cash options.

What Is a Treasury Bill?

A Treasury bill (T-bill) is a short-term security issued by the U.S. government.

When you buy one, you are lending money to the U.S. Treasury for a set period of time. In return, the government promises to repay the bill’s full face value when it matures.

Unlike many other fixed-income investments, Treasury bills do not usually make periodic interest payments.

Instead, they are sold for less than their face value, and your return comes from the difference between:

- the price you pay today

- the amount you receive at maturity

That is why T-bills are often described as being sold at a discount.

A Treasury bill is not designed to make you rich quickly.

It is designed to help you manage cash with a defined time horizon.

How Does a Treasury Bill Work?

Treasury bills are straightforward.

You buy the bill below face value, hold it until maturity, and receive the full amount at the end.

Simple example

Suppose you buy a T-bill with a face value of $10,000 for $9,800.

At maturity, the U.S. Treasury pays you $10,000.

Your profit is:

- $10,000 - $9,800 = $200

That $200 is your return.

So while a T-bill does not pay interest in the traditional coupon-paying sense, it still produces income through the discount between purchase price and maturity value.

Estimate your own T-Bill return

If you know the amount you want to invest and the maturity you are considering, use the calculator to estimate your potential return.

Common Treasury Bill Maturities

Treasury bills are designed for short-term time horizons, not long-term investing.

Common maturities include:

- 4 weeks

- 8 weeks

- 13 weeks

- 17 weeks

- 26 weeks

- 52 weeks

Because the maturities are short, T-bills are commonly used for:

- temporary cash parking

- emergency fund planning

- short-term savings goals

- business reserve cash

- tax reserves

- Treasury ladder strategies

If your time horizon is only a few weeks or months, T-bills are often more relevant than long-term bonds.

If your time horizon is years or decades, T-bills may still have a role, but they are usually not the main growth engine.

Why Investors Use Treasury Bills

Treasury bills are not attractive because they are exciting.

They are attractive because they solve a specific problem:

How do you keep cash relatively safe while still earning something on it?

1. Safety

Treasury bills are backed by the full faith and credit of the U.S. government.

That is why they are widely viewed as among the safest U.S. dollar-denominated investments available.

Safety, however, does not mean they are perfect for every purpose. It means the credit risk is very low compared with most other investments.

2. Predictability

If you hold a T-bill until maturity, you know in advance:

- when it will mature

- the face value scheduled to be paid at maturity

- the structure of your return

That makes T-bills easier to plan around than volatile assets.

3. Short-term flexibility

Because maturities are short, T-bills can fit cash you may need soon.

For example, someone saving for a tax payment in three months may prefer a short-term T-bill over committing money to a longer-term investment.

4. State and local tax advantage

Interest from Treasury securities is generally exempt from state and local income taxes.

That can make T-bills more attractive than some alternatives for investors in higher-tax states.

This does not mean Treasury bills always beat savings accounts or CDs. It means the after-tax comparison may be different from the headline yield comparison.

How Investors Actually Make Money From T-Bills

A lot of beginners assume a Treasury bill works like a savings account.

It does not.

A savings account usually credits interest over time.

A T-bill usually works through discount pricing.

That means your return depends on:

- your purchase price

- the face value

- the time until maturity

- the yield available when you buy

In practical terms, if yields rise, newly issued T-bills usually become more attractive.

If yields fall, new bills usually offer less.

That is why investors often watch current T-bill yields before deciding when and how long to invest.

👉 You can check current market levels here:

View Treasury Rates

What Affects Treasury Bill Yields?

Treasury bill yields change constantly based on market conditions.

Several forces influence them.

Federal Reserve policy

Short-term Treasury yields are heavily influenced by the broader interest-rate environment, including expectations around Federal Reserve policy.

Inflation expectations

If inflation is expected to stay elevated, investors usually demand higher yields to compensate for reduced purchasing power.

Demand for safety

During periods of uncertainty, strong demand for safe assets can affect Treasury pricing and yields.

Time to maturity

A 4-week bill and a 52-week bill may not offer the same yield.

The maturity you choose affects both your potential return and your flexibility.

Treasury Bills vs Savings Accounts

Treasury bills and savings accounts are often compared because both are used for cash rather than long-term speculation.

But they serve different roles.

| Feature | Treasury Bills | High-Yield Savings Accounts |

|---|---|---|

| Backing/protection | U.S. government | FDIC/NCUA insurance when held at an insured institution, subject to limits |

| Return structure | Discount to face value | Ongoing interest/APY |

| Liquidity | Best when held to maturity; can be sold early but may involve price risk or inconvenience | Usually immediate or near-immediate |

| Term | Fixed maturity | Open-ended |

| Rate behavior | Locked for that bill at purchase | Can change anytime |

| State/local tax treatment | Generally exempt from state and local income tax | Usually taxable where applicable |

| Best use case | Planned cash for a set period | Daily access cash and emergency liquidity |

A savings account usually wins on instant access.

A T-bill may win when you can leave money alone until maturity and want a more structured way to earn on cash.

👉 Compare both side by side here:

Compare T-Bills vs Savings

Treasury Bills vs Other Investments

Treasury bills are best understood as a cash management tool, not a growth engine.

| Investment Type | Risk Level | Return Potential | Typical Use |

|---|---|---|---|

| Treasury Bills | Very low credit risk | Low to moderate | Short-term cash |

| Savings Account | Very low when insured | Low | Emergency liquidity |

| Certificates of Deposit | Low when insured | Low to moderate | Cash with a set time horizon |

| Corporate Bonds | Moderate | Moderate | Income with more credit risk |

| Stocks | High | Higher long-term potential | Long-term growth |

If your goal is to maximize wealth over decades, T-bills alone are usually not enough.

If your goal is to protect cash you may need soon, they can be very useful.

Risks and Limitations of Treasury Bills

Treasury bills are very safe from a credit-risk perspective, but that does not mean they are perfect.

Inflation risk

Even if your principal repayment is highly predictable, inflation may reduce what your money can buy by the time the bill matures.

Opportunity cost

If stock markets, business opportunities, or other investments perform much better, T-bills may look conservative in comparison.

That is not necessarily bad. It depends on the job you assigned to the cash.

Access risk before maturity

If you need the money early, you may have to sell before maturity if you did not structure your cash well in advance.

That may be inconvenient, and the sale price can depend on market conditions.

Reinvestment risk

If rates fall later, the next T-bill you buy may offer a lower yield than the one you just held.

These are not reasons to avoid T-bills.

They are reasons to use them intentionally.

Who Should Consider Treasury Bills?

Treasury bills may make sense for people who:

- want to earn something on idle cash

- have a known short-term time horizon

- want to reduce risk

- are building a conservative cash strategy

- want an alternative to leaving too much money in checking

- want to organize cash by maturity date

They are especially useful for money you do not need today, but may need in a few weeks or months.

Examples:

- emergency fund layers

- upcoming tuition payments

- tax reserves

- home purchase funds with a near-term closing date

- business operating reserves

- cash set aside for a known future expense

Not sure which maturity fits your cash?

Start with current Treasury rates, then estimate how much a T-bill could return over your expected holding period.

Who Should Not Rely on T-Bills for Everything?

Treasury bills are not ideal for every purpose.

They may be a poor fit if:

- you need the money at any moment

- you are investing for very long-term growth

- you cannot tolerate tying cash up for a fixed period

- your cash flow is unpredictable and you may need instant access

- you do not want to track maturity dates or reinvestment decisions

In those cases, a savings account or a blended cash strategy may be more practical.

A common approach is to keep immediate cash in savings and use Treasury bills only for the portion of cash with a clearer timeline.

How to Buy Treasury Bills

You can buy Treasury bills in a few common ways.

1. TreasuryDirect

TreasuryDirect lets you buy directly from the U.S. Treasury.

This can be useful for investors who want direct ownership and do not need a brokerage interface.

2. Brokerage account

Many brokers let you buy new Treasury issues or existing Treasury securities.

This can be convenient if you already manage investments in a brokerage account.

3. Treasury-focused ETFs or funds

Treasury-focused ETFs and funds can provide exposure to Treasury bills or short-term Treasuries.

However, they are not exactly the same thing as holding an individual bill to maturity.

Funds can be easier to trade, but their prices and yields can move differently from a single T-bill held to maturity.

For many investors, the best approach depends on whether they want direct ownership, easier account management, or more flexibility.

How to Estimate Your Return

Before buying a T-bill, it helps to estimate:

- how much you plan to invest

- the current yield

- the maturity you are considering

- how long you plan to hold it

- whether state and local tax treatment matters in your situation

A small yield difference can matter when you are working with larger cash balances.

👉 Estimate your return here:

Use the T-Bill Calculator

Using Treasury Bills in a Ladder Strategy

One of the most useful ways to use Treasury bills is through a ladder.

A ladder spreads your cash across multiple maturities so that part of your money becomes available at regular intervals.

This can help balance:

- yield

- liquidity

- flexibility

- reinvestment timing

For example, instead of putting all your cash into one 26-week bill, you might spread it across several maturities so money is coming due more often.

A ladder can be useful when you want to earn on cash but do not want everything locked into one maturity date.

👉 Learn more here:

How to Build a Treasury Ladder

Or try the tool directly:

Use the Ladder Builder

A Practical Way to Decide Whether a T-Bill Makes Sense

Ask yourself these questions:

- When will I need this money?

- Can I wait until the bill matures?

- Do I need immediate liquidity, or can this cash be scheduled?

- Am I trying to protect cash, grow cash, or simply earn more than checking?

- Would state and local tax treatment affect the comparison?

- Do I want one maturity date or a ladder of maturities?

If the money has a known timeline, a Treasury bill may fit.

If the money may be needed at any moment, a savings account may be better.

If you want both structure and flexibility, a blended approach may make more sense.

Frequently Asked Questions

Are Treasury bills safe?

Treasury bills are widely considered among the safest U.S. dollar investments because they are backed by the U.S. government.

That said, investors should still think about inflation, liquidity, and opportunity cost.

Do Treasury bills pay monthly interest?

No.

Treasury bills usually do not make periodic interest payments.

Investors typically earn the difference between the discounted purchase price and the face value received at maturity.

Can I lose money in a Treasury bill?

If you hold a Treasury bill to maturity, the repayment structure is highly predictable.

However, if you sell before maturity, the price you receive can depend on market conditions.

Inflation and opportunity cost can also reduce the real value of your return.

Are Treasury bills better than a savings account?

Not always.

T-bills may offer advantages for planned short-term cash, especially when you can wait until maturity.

Savings accounts usually offer more immediate access and may be better for emergency cash.

What is the shortest Treasury bill maturity?

Treasury bills are commonly issued in very short maturities, including 4-week bills.

Are Treasury bills good for an emergency fund?

They can be useful for part of an emergency fund, but usually not all of it.

Many people prefer to keep immediate emergency cash in a savings account and use T-bills only for the portion of cash they are less likely to need right away.

Do Treasury bills have state income tax advantages?

Interest from Treasury securities is generally exempt from state and local income taxes.

That can make the after-tax return more attractive for investors in higher-tax states.

Final Thought

A Treasury bill is one of the simplest tools in finance, but it is also one of the most useful.

It gives you a way to put cash to work without reaching for unnecessary risk.

That is why T-bills are not just an investment product.

They are a cash management tool.

If you understand how they work, when to use them, and where they fit in your overall financial system, they can help you make better short-term money decisions.

The goal is not to put every dollar into Treasury bills.

The goal is to match each dollar with the right job.

Some cash needs immediate access.

Some cash has a known timeline.

Treasury bills are most useful for the second category.

Next Step

Choose the next step based on what you are trying to do.

If you want to check current T-Bill yields

Start with the live rates page to see where Treasury rates are today.

If you want to estimate a T-Bill return

Use the calculator to estimate potential return for a specific amount and maturity.

If you want to compare T-Bills with savings

Compare Treasury bills against high-yield savings accounts using current rates and practical cash-management tradeoffs.

If you want recurring access to cash

Learn how a Treasury ladder can spread maturities over time.

How to Build a Treasury Ladder

Build a Treasury Ladder

If you want the broader picture

Learn how Treasury bills fit into the larger family of U.S. Treasury securities.