What Are US Treasury Securities? A Complete Guide to Treasury Bills, Notes, Bonds, TIPS, FRNs, and STRIPS

Learn what US Treasury securities are, how they work, and how Treasury bills, notes, bonds, TIPS, floating rate notes, and STRIPS compare.

Most people hear the phrase US Treasury securities and assume it refers to a single product.

It does not.

US Treasury securities are a family of government-issued debt instruments, and each one is built for a different purpose.

Some are designed for short-term cash management.

Some are built for steady income over several years.

Some are designed to help protect purchasing power from inflation.

Others are structured for specific future payout dates.

That is why understanding the differences matters.

The right Treasury security depends on what you need your money to do.

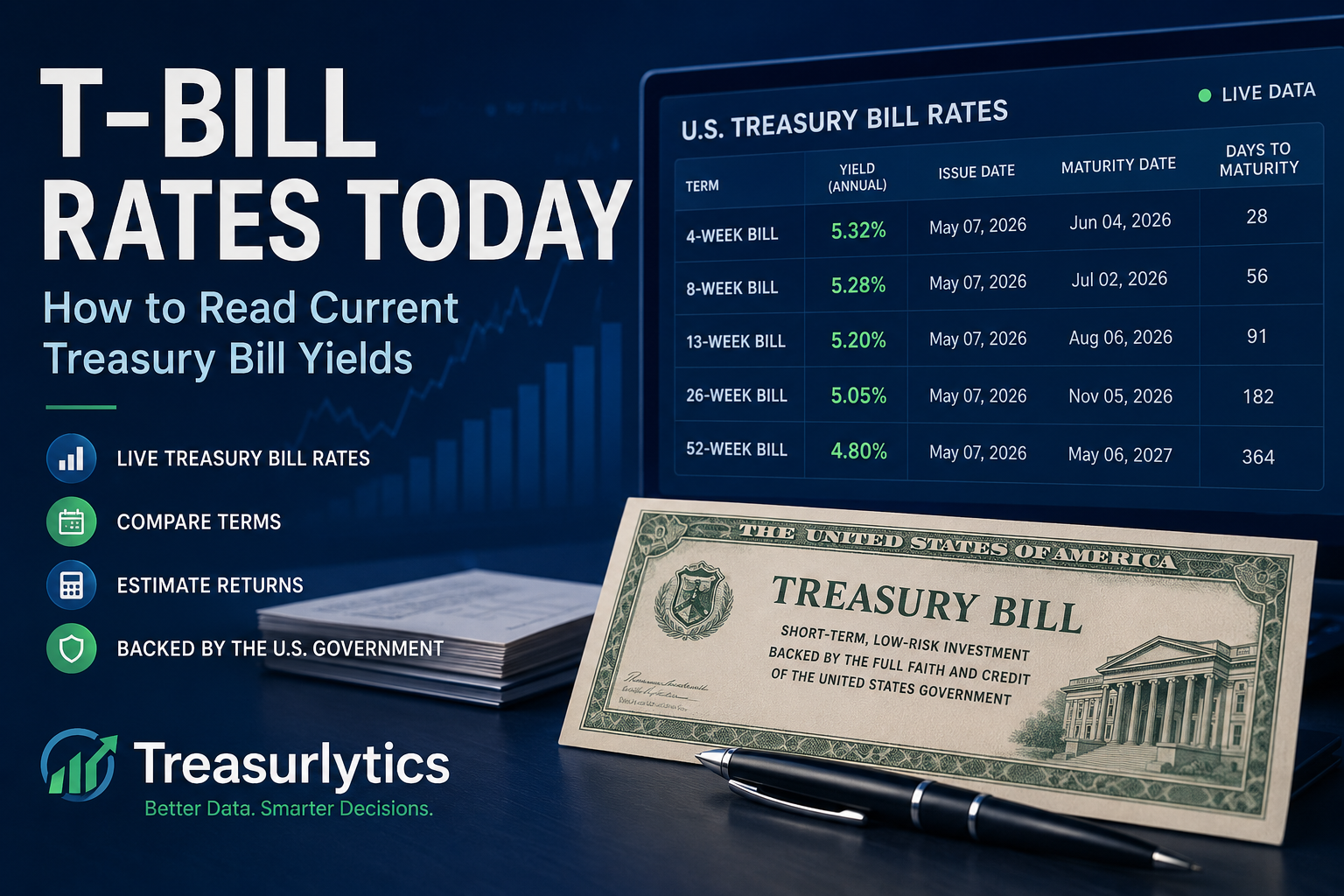

Start with current Treasury yields

Before choosing between Treasury bills, notes, bonds, TIPS, FRNs, or STRIPS, it helps to see where current Treasury yields are today.

What Are US Treasury Securities?

US Treasury securities are debt instruments issued by the United States Department of the Treasury to help finance government operations.

When you buy one, you are effectively lending money to the U.S. government.

In return, the government agrees to repay you according to the terms of that specific security.

These securities are widely viewed as among the safest investments in the world because they are backed by the full faith and credit of the United States.

That does not mean they are all identical.

They differ in:

- maturity length

- payment structure

- inflation exposure

- interest rate sensitivity

- liquidity profile

- best use case

Understanding those differences is what turns “Treasuries” from a vague safe-investment idea into an actual strategy.

Why Treasury Securities Matter

US Treasury securities matter for much more than individual investing.

They play a major role in both personal finance and the broader global financial system.

They are used by:

- individual investors seeking safety

- institutions managing large pools of cash

- retirement portfolios looking for stability

- banks and funds needing highly liquid assets

- global markets as a benchmark for interest rates

Treasuries help define what “risk-free” means in many parts of finance.

That is why Treasury yields influence everything from savings decisions to mortgage rates to stock valuations.

They are not just investments.

They are part of the financial system’s foundation.

For everyday investors, the important point is simpler:

Treasury securities can help you match money with a specific timeline, purpose, and risk level.

The Main Types of US Treasury Securities

The major categories include:

- Treasury Bills (T-Bills)

- Treasury Notes (T-Notes)

- Treasury Bonds (T-Bonds)

- Treasury Inflation-Protected Securities (TIPS)

- Floating Rate Notes (FRNs)

- STRIPS

Each one has a different maturity structure, payment method, and use case.

👉 Compare current yields for each type:

View Live Treasury Rates

Treasury Bills (T-Bills)

Treasury bills are short-term securities with maturities of up to one year.

They do not make regular interest payments.

Instead, they are sold at a discount and mature at full face value.

Example

- Buy for $9,800

- Mature at $10,000

- Profit = $200

T-bills are best for:

- short-term cash management

- parking money safely

- emergency fund layers

- near-term spending goals

- tax reserves

- investors who want minimal interest rate risk

Because their maturities are short, T-bills are often the most practical Treasury product for people managing cash they may need in a few weeks or months.

Estimate short-term T-Bill returns

If you are considering a 4-week, 13-week, 26-week, or 52-week Treasury bill, use the calculator to estimate your potential return.

👉 Learn more here:

What Is a Treasury Bill?

Treasury Notes (T-Notes)

Treasury notes are medium-term securities.

They pay fixed interest every six months and return principal at maturity.

Typical maturities include:

- 2 years

- 3 years

- 5 years

- 7 years

- 10 years

Treasury notes are often used by investors who want:

- more duration than short-term bills

- less duration risk than long bonds

- predictable income over several years

- exposure to intermediate-term Treasury yields

They sit in the middle of the Treasury spectrum.

That makes them useful for investors who want something more stable than long-term bonds, but less short-dated than Treasury bills.

Treasury Bonds (T-Bonds)

Treasury bonds are long-term securities.

Like notes, they pay fixed interest every six months, but they have much longer maturities:

- 20 years

- 30 years

Treasury bonds are best for:

- long-term income

- retirement planning

- liability matching

- portfolio stability

Because they have longer maturities, Treasury bonds usually carry more interest rate risk than bills or notes.

That means their market prices tend to move more when interest rates change.

They can still be useful, but they are generally a bigger commitment than shorter-term Treasury instruments.

If you may need the money soon, long-term Treasury bonds are usually not the first place to look.

Treasury Inflation-Protected Securities (TIPS)

TIPS are designed to help protect investors from inflation.

They pay interest every six months, but their principal adjusts based on changes in inflation.

That means:

- when inflation rises, the principal value of the security increases

- when inflation falls, the principal can decrease

- interest payments change because they are based on the adjusted principal

TIPS are useful for investors who want:

- inflation protection

- real purchasing power preservation

- a hedge against rising prices

TIPS are not necessarily about maximizing nominal return.

They are about protecting real value.

That makes them especially relevant when inflation is a bigger concern than simply locking in a fixed nominal yield.

Floating Rate Notes (FRNs)

Floating Rate Notes are Treasury securities whose interest payments reset periodically rather than staying fixed.

Instead of locking in one coupon rate for the entire life of the security, FRNs move with short-term interest rate conditions.

This makes them useful when:

- interest rates are changing

- investors want less duration risk than fixed-rate notes or bonds

- investors want government-backed exposure with variable income

- investors do not want to commit fully to a fixed coupon

FRNs can appeal to investors who do not want to lock into a fixed rate when the rate environment is uncertain.

They are often thought of as a more adaptive alternative to traditional fixed-rate Treasury securities.

STRIPS

STRIPS stands for Separate Trading of Registered Interest and Principal of Securities.

STRIPS are created by separating the interest payments and principal of a Treasury note or bond into individual zero-coupon securities.

This means:

- no periodic interest payments

- each strip is purchased at a discount

- the investor receives a lump sum at maturity

STRIPS are commonly used for:

- future liability matching

- locking in a known future value

- long-term planning for specific dates

Because they do not pay periodic interest, STRIPS can be more sensitive to interest rate changes than regular coupon-paying securities of similar maturity.

They are powerful planning tools, but they are generally more specialized than standard Treasury bills, notes, or bonds.

Quick Comparison Table

👉 Want to see how these compare right now?

View Live Treasury Rates

| Security Type | Typical Maturity | Payment Style | Inflation Protection | Interest Rate Sensitivity | Best For |

|---|---|---|---|---|---|

| Treasury Bills | 4 weeks to 1 year | No coupon; sold at discount | No | Very low | Short-term cash |

| Treasury Notes | 2 to 10 years | Fixed interest every 6 months | No | Moderate | Medium-term income |

| Treasury Bonds | 20 to 30 years | Fixed interest every 6 months | No | High | Long-term income |

| TIPS | 5, 10, and 30 years commonly | Fixed rate on inflation-adjusted principal | Yes | Moderate to high | Inflation protection |

| FRNs | Short to medium term | Floating rate resets | No | Low to moderate | Changing-rate environments |

| STRIPS | Varies based on original security | No coupon; zero-coupon | No | High | Future lump-sum goals |

Treasury Bills vs Notes vs Bonds

Treasury bills, notes, and bonds are the core fixed-income Treasury categories, but they serve very different purposes.

| Feature | Treasury Bills | Treasury Notes | Treasury Bonds |

|---|---|---|---|

| Time Horizon | Short-term | Medium-term | Long-term |

| Typical Maturity | 4 weeks to 1 year | 2 to 10 years | 20 to 30 years |

| Coupon Payments | None | Yes | Yes |

| Main Return Source | Discount to face value | Fixed coupon + principal | Fixed coupon + principal |

| Rate Risk | Lowest | Moderate | Highest |

| Ideal Use | Cash parking | Balanced income | Long-term income |

A simple way to think about them:

- Bills = short-term safety

- Notes = middle-ground income

- Bonds = long-term income commitment

If your money has a near-term job, bills are usually the most relevant.

If you want fixed income over a few years, notes may make more sense.

If you are making a long-term allocation decision, bonds are more likely to be in the conversation.

TIPS vs Fixed-Rate Treasuries

TIPS and standard Treasuries may look similar at first, but their purpose is different.

| Feature | TIPS | Treasury Notes/Bonds |

|---|---|---|

| Inflation Adjustment | Yes | No |

| Coupon Type | Fixed rate on adjusted principal | Fixed rate on original principal |

| Main Goal | Preserve real purchasing power | Generate nominal income |

| Best In | Higher inflation environments | Stable or lower inflation environments |

If your biggest concern is inflation, TIPS are usually more relevant than standard notes or bonds.

If your primary goal is fixed nominal income, traditional notes and bonds are usually simpler.

FRNs vs Treasury Bills

FRNs and T-bills can both appeal to conservative investors, but they behave differently.

| Feature | FRNs | Treasury Bills |

|---|---|---|

| Coupon Structure | Floating | None |

| Yield Behavior | Resets with short-term rates | Locked at purchase |

| Rate Risk | Low | Very low |

| Reinvestment Need | Less frequent | More frequent for ongoing exposure |

| Best For | Variable-rate exposure | Simplicity and short-term certainty |

T-bills are simpler.

FRNs are more adaptive.

That makes T-bills a common choice for straightforward short-term cash planning, while FRNs may appeal more to investors who want variable-rate exposure without moving too far out on the risk spectrum.

STRIPS vs Traditional Treasury Bonds

Although STRIPS are derived from Treasury notes or bonds, they behave differently in a portfolio.

| Feature | STRIPS | Treasury Bonds |

|---|---|---|

| Coupon Payments | None | Semiannual |

| Cash Flow Pattern | One payment at maturity | Regular income + principal |

| Duration Sensitivity | Higher | Lower than comparable STRIPS |

| Best For | Specific future lump-sum goals | Ongoing income |

STRIPS can be powerful planning tools, but they are usually not the first Treasury product most beginners should start with.

Which Treasury Security Is Best?

There is no single best Treasury security.

The better question is:

Best for what?

Choose Treasury Bills if you want:

- short-term safety

- predictable maturity in under 1 year

- a place to park cash

- a tool for planned short-term expenses

Choose Treasury Notes if you want:

- fixed income over a few years

- a balance between yield and flexibility

- less duration risk than long bonds

- medium-term Treasury exposure

Choose Treasury Bonds if you want:

- long-term income

- stability in a conservative portfolio

- exposure to longer-term government yields

- a longer-duration fixed-income allocation

Choose TIPS if you want:

- inflation protection

- better preservation of real value

- a hedge against rising prices

- Treasury exposure linked to inflation adjustments

Choose FRNs if you want:

- variable-rate income

- reduced concern about locking into fixed rates

- government-backed exposure in a changing rate environment

Choose STRIPS if you want:

- a future lump sum on a specific date

- zero-coupon planning tools

- precision for liability matching

The best Treasury security depends on your timeline, income needs, liquidity needs, and view of inflation and interest rates.

For short-term cash, start with T-Bills

If your main goal is parking cash for weeks or months, Treasury bills are usually the simplest place to start.

How Investors Use Treasury Securities Together

Many investors do not choose just one Treasury instrument.

They combine them.

Examples:

- Bills + Notes for cash plus medium-term income

- Notes + Bonds for a more stable income ladder

- Bills + TIPS for liquidity plus inflation protection

- FRNs + Bills in uncertain rate environments

- STRIPS for targeted long-term obligations

Using multiple Treasury securities together can help align money with different time horizons and financial goals.

For example, someone might keep near-term reserves in T-bills, longer-term conservative assets in notes, and add TIPS for inflation defense.

Treasuries work best when matched to the job each dollar is supposed to do.

Treasury Securities and Risk

Although Treasury securities are considered very safe from a credit risk standpoint, they are not all equally risk-free in practice.

Different kinds of Treasury risk include:

Interest rate risk

Longer maturities are more sensitive to changing rates.

If rates rise, the market value of existing longer-term bonds may fall.

Inflation risk

Fixed-rate securities can lose purchasing power if inflation rises faster than expected.

Reinvestment risk

Shorter-term securities may need to be reinvested at lower future yields.

Liquidity trade-offs

Although Treasuries are generally liquid, your investment strategy still matters if you may need money before maturity.

Safety is not just about avoiding default.

It is also about matching the instrument to the job.

That distinction matters a lot.

A Treasury security can be very safe from default risk and still be a poor choice for your specific goal if the maturity, inflation exposure, or cash flow pattern does not match your needs.

How Treasury Securities Fit Into a Cash and Investing Strategy

Treasury securities can be used in very different ways depending on your objective.

For cash management

Treasury bills and FRNs are often most relevant.

For portfolio stability

Treasury notes and bonds can provide balance.

For inflation defense

TIPS are the most direct Treasury option.

For future lump-sum planning

STRIPS can provide precision.

The category is broad because investor needs are broad.

The more clearly you define the purpose of your money, the easier it becomes to decide which Treasury security fits.

Using Treasury Securities for Cash Management

For many everyday investors, the most practical use of Treasury securities is not advanced bond portfolio construction.

It is cash management.

That means using Treasuries to organize money by timeline.

For example:

- money needed in the next few weeks may stay in savings

- money needed in 1 to 3 months may fit a short T-bill

- money needed in 3 to 12 months may fit a longer T-bill or ladder

- longer-term conservative money may fit notes, bonds, or TIPS

Treasury bills are especially useful because they let investors turn idle cash into time-based cash.

Instead of asking, “Where can I get the highest yield?”

A better question is:

When do I need this money back?

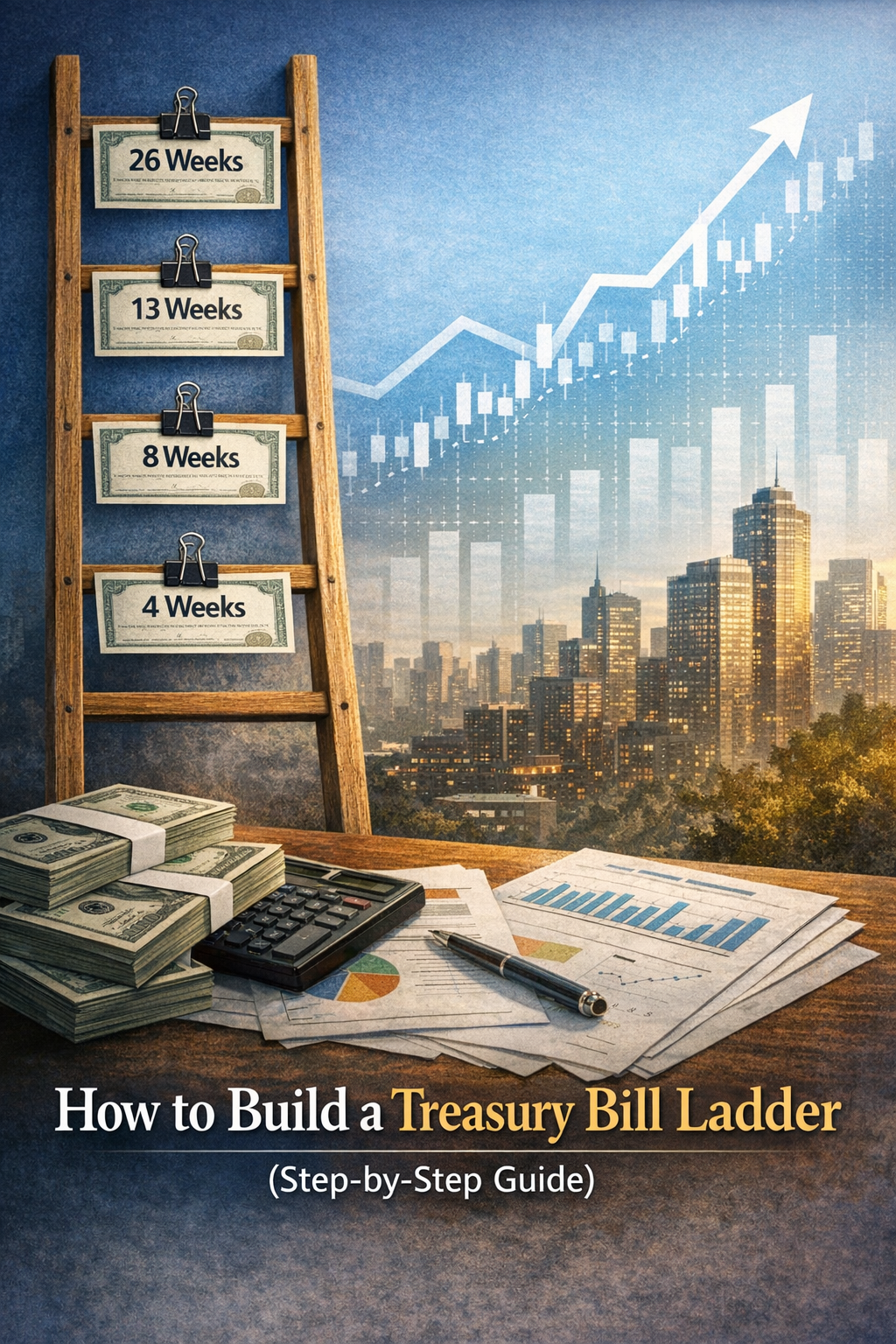

Build a Treasury ladder for recurring access

If you want part of your money becoming available on a regular schedule, a ladder can help spread maturities over time.

Frequently Asked Questions

Are US Treasury securities safe?

They are widely considered among the safest U.S. dollar investments from a credit-risk standpoint because they are backed by the U.S. government.

However, different Treasury securities still carry different levels of inflation risk, interest rate risk, and reinvestment risk.

What is the difference between a Treasury bill and a Treasury note?

A Treasury bill is short term and does not usually pay periodic coupons.

A Treasury note has a longer maturity and typically pays fixed interest every six months.

What Treasury security protects against inflation?

TIPS are specifically designed to provide inflation protection by adjusting principal based on inflation.

Are Treasury bonds better than Treasury bills?

Not necessarily.

Bonds are generally more suitable for long-term income needs, while bills are usually better for short-term cash management.

The right choice depends on your timeline.

What are STRIPS used for?

STRIPS are often used when an investor wants a known lump sum at a specific future date.

They are more specialized than regular Treasury bills, notes, or bonds.

Which Treasury security is best for short-term cash?

Treasury bills are usually the most practical Treasury security for short-term cash because they have short maturities and simple return mechanics.

Which Treasury security is best for inflation protection?

TIPS are designed specifically for inflation protection because their principal adjusts based on inflation.

Next Step

Now that you understand how each Treasury security works, choose the next step based on your goal.

If you want to see current Treasury yields

Start with the live rates page to compare current yields across Treasury securities.

If you want to focus on short-term cash

Learn how Treasury bills work and estimate potential short-term returns.

What Is a Treasury Bill?

Use the T-Bill Calculator

If you want to compare T-Bills with savings

Compare Treasury bills against high-yield savings accounts as cash-management options.

If you want recurring access to cash

Learn how a Treasury ladder can spread maturities over time.

How to Build a Treasury Ladder

Build a Treasury Ladder

Final Thought

US Treasury securities are not one product.

They are a toolkit.

Treasury bills, notes, bonds, TIPS, floating rate notes, and STRIPS all serve different purposes.

Understanding those differences is what turns a generic “safe investment” idea into a real strategy.

The goal is not just to buy something backed by the government.

The goal is to choose the Treasury security that matches your timeline, income needs, inflation concerns, liquidity needs, and risk tolerance.

When used thoughtfully, Treasury securities can help you manage cash more efficiently, reduce risk in a portfolio, and make your overall financial plan more resilient.