Treasury Bills vs High-Yield Savings: Which Should You Use in 2026?

Compare Treasury bills and high-yield savings accounts, including liquidity, yield behavior, taxes, and when each option makes the most sense for your cash.

When it comes to managing cash, many people default to a savings account.

That makes sense.

A savings account is familiar, simple, and easy to access.

But it is not always the most efficient home for every dollar you hold.

Treasury bills offer another option. In some situations, they can provide a stronger return, a more predictable maturity date, and a better fit for short-term cash you do not need immediately.

The real question is not which one is universally better.

The better question is:

Which one fits this specific piece of cash?

That is the key idea.

Treasury bills and high-yield savings accounts are not direct enemies. They are different tools for different jobs.

Compare T-Bills vs High-Yield Savings

Before deciding where to park your cash, compare current Treasury yields against savings rates using real numbers.

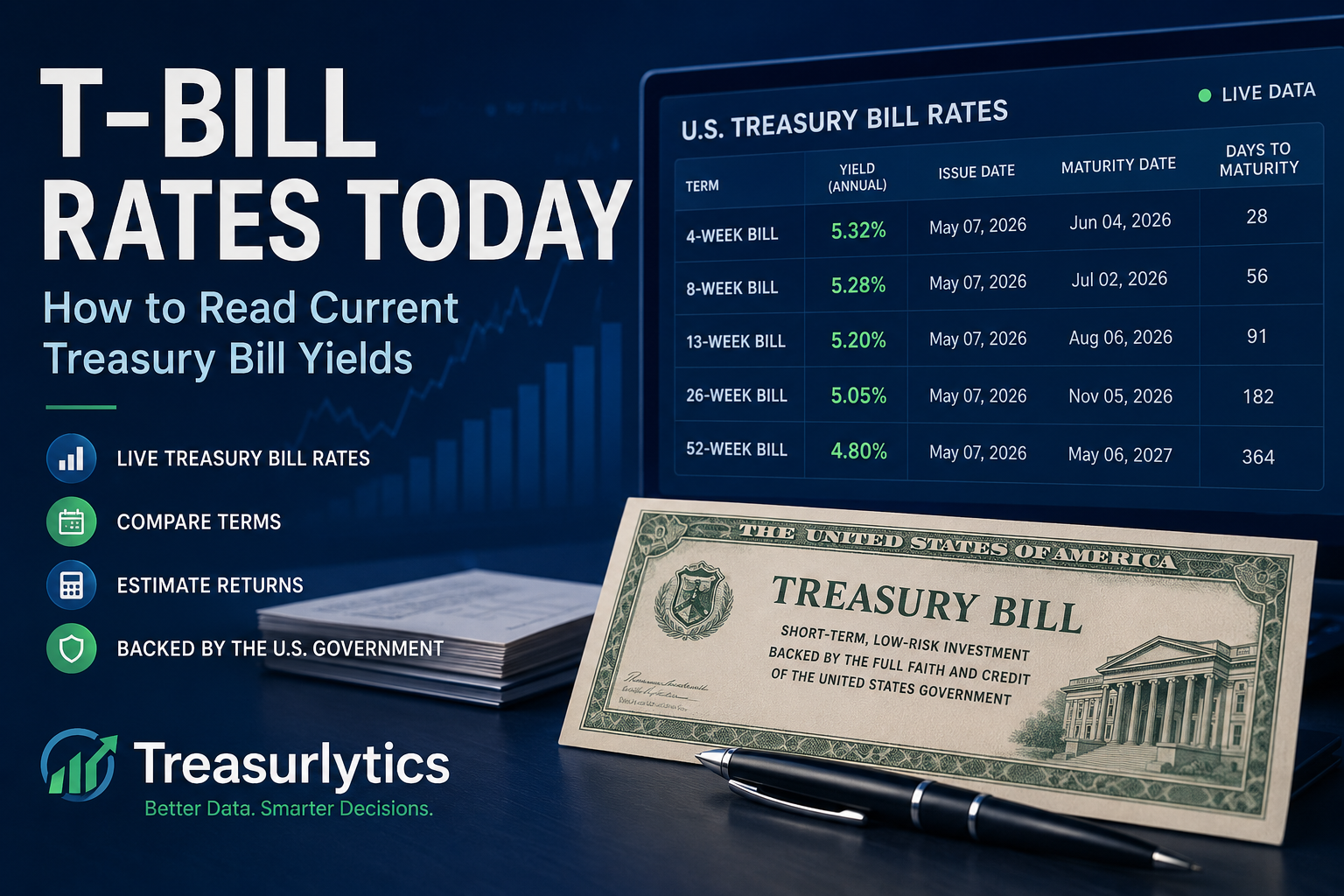

What Is a Treasury Bill?

A Treasury bill, or T-bill, is a short-term security issued by the U.S. Treasury.

It is usually sold at a discount and matures at full face value.

That means your return comes from the difference between:

- what you pay today

- and what you receive at maturity

Common T-bill durations include:

- 4 weeks

- 8 weeks

- 13 weeks

- 17 weeks

- 26 weeks

- 52 weeks

When you buy a T-bill, you know the maturity date in advance.

That makes Treasury bills useful for cash that has a known time horizon.

👉 Learn more here:

What Is a Treasury Bill?

What Is a High-Yield Savings Account?

A high-yield savings account is a bank account that pays interest on your balance while keeping your money relatively accessible.

Unlike a Treasury bill, a savings account does not have a fixed maturity date.

Your money stays available, and the interest rate can change at any time.

That flexibility is a major advantage.

A high-yield savings account is often best for cash that needs to remain immediately or unpredictably available.

Treasury Bills vs Savings Accounts: The Core Difference

The biggest difference is simple:

- a savings account prioritizes access

- a Treasury bill prioritizes structure and predictability

A savings account is open-ended.

A Treasury bill has a fixed term.

A savings account usually gives you immediate access to cash.

A Treasury bill gives you a defined maturity date and a locked-in yield for that holding period.

That means the right choice often depends less on the interest rate alone and more on when you may need the money.

Quick Comparison Table

| Feature | Treasury Bills | High-Yield Savings Accounts |

|---|---|---|

| Backing/protection | U.S. government | FDIC/NCUA insurance when held at an insured institution, subject to limits |

| Access to cash | At maturity unless sold early | Usually immediate |

| Rate behavior | Locked at purchase for that bill | Can change anytime |

| Term | Fixed | Open-ended |

| Return structure | Discount to face value | Ongoing APY |

| State/local tax treatment | Generally exempt from state and local income tax | Usually taxable where applicable |

| Best use case | Planned short-term cash | Immediate-access cash |

1. Liquidity

Liquidity is where savings accounts usually win.

Savings accounts

Your money is generally available right away or within a very short time.

That makes savings accounts useful for:

- emergency cash

- irregular expenses

- uncertain short-term needs

- cash you may need without warning

Treasury bills

Treasury bills are designed to be held until maturity.

If you need the money early, you may have to sell before maturity, which can introduce price risk or inconvenience.

If you might need the cash unexpectedly, savings accounts are usually the safer choice from a liquidity standpoint.

2. Yield Behavior

Treasury bills and savings accounts also behave differently when it comes to returns.

Savings accounts

Savings rates can move up or down whenever the bank decides to change them.

That means your return is flexible, but not guaranteed at one level.

Treasury bills

When you buy a Treasury bill, the yield for that holding is effectively locked in at purchase.

That gives you more predictability.

This is one of the biggest advantages of T-bills for planned short-term cash.

You know the maturity date, and you know the approximate return structure from the start.

👉 Compare current levels here:

Compare Treasury Yields vs Savings Rates

You can also check the latest Treasury rate data before comparing options:

View Live Treasury Rates

3. Taxes

Taxes can change the comparison more than many people expect.

Interest from Treasury securities is generally exempt from state and local income taxes, while savings account interest is usually taxable at the federal, state, and local level where applicable.

That means a Treasury bill can sometimes be more attractive on an after-tax basis, especially for someone living in a higher-tax state.

This does not mean T-bills always win.

But it does mean the stated rate alone does not tell the full story.

4. Simplicity vs Planning

Savings accounts are simpler.

You open the account, deposit money, and keep it available.

Treasury bills require a bit more planning.

You need to decide:

- how much to invest

- which maturity to choose

- whether you may need the money before maturity

- whether you want to reinvest later

For some people, that extra structure is a disadvantage.

For others, it is exactly what makes T-bills useful.

A Treasury bill forces you to assign a job and a timeline to your cash.

When Treasury Bills May Be Better

Treasury bills may make more sense if:

- you know you will not need the money for a specific period

- you want a defined maturity date

- you want a more predictable short-term return

- you are organizing cash by time horizon

- you want to improve after-tax cash efficiency

Examples:

- cash needed in 3 months → a 13-week T-bill

- cash needed in 6 months → a 26-week T-bill

- business reserve cash with known timing → a short-term ladder

- tax money you know you will owe later → a matched maturity

Estimate your potential T-Bill return

If you are considering a 13-week or 26-week Treasury bill, use the calculator to estimate the purchase price, maturity value, and expected return.

Treasury bills work best when the cash has a job, but that job starts later.

When Savings Accounts May Be Better

Savings accounts may make more sense if:

- you need immediate liquidity

- your timeline is uncertain

- you want maximum simplicity

- the money may need to move quickly

- you do not want to manage maturity dates

Examples:

- emergency fund core cash

- rent or near-term bills

- irregular household expenses

- money you may need unexpectedly this week or next month

In these cases, flexibility matters more than squeezing out every possible bit of yield.

Real-Life Use Cases

Emergency fund

A savings account is usually better for the portion of your emergency fund that must be available immediately.

A Treasury bill may work for the portion you are less likely to need right away.

Home down payment fund

If you know the purchase timeline is a few months away, Treasury bills may fit better than leaving everything in savings.

If the purchase timing is uncertain, savings may be safer.

Tax reserve

Treasury bills can be a strong option for tax money you know you will owe on a future date.

Business reserve cash

If part of the reserve is unlikely to be used immediately, Treasury bills or a ladder may help put that cash to work more efficiently.

A Hybrid Approach Often Works Best

For many people, the best solution is not choosing one or the other.

It is using both.

A practical cash strategy often looks like this:

- keep immediately accessible cash in savings

- move predictable, time-bound cash into Treasury bills

- use a ladder if you want recurring access points

This creates a balance between:

- liquidity

- structure

- predictability

- yield potential

That is often a better framework than asking which one is “better” in the abstract.

Turn this article into a practical checklist

If you are deciding how to split money between savings, T-bills, and a Treasury ladder, start by checking the current rates and then estimate the return on the portion of cash you can lock up.

Treasury Bills, Savings Accounts, and Treasury Ladders

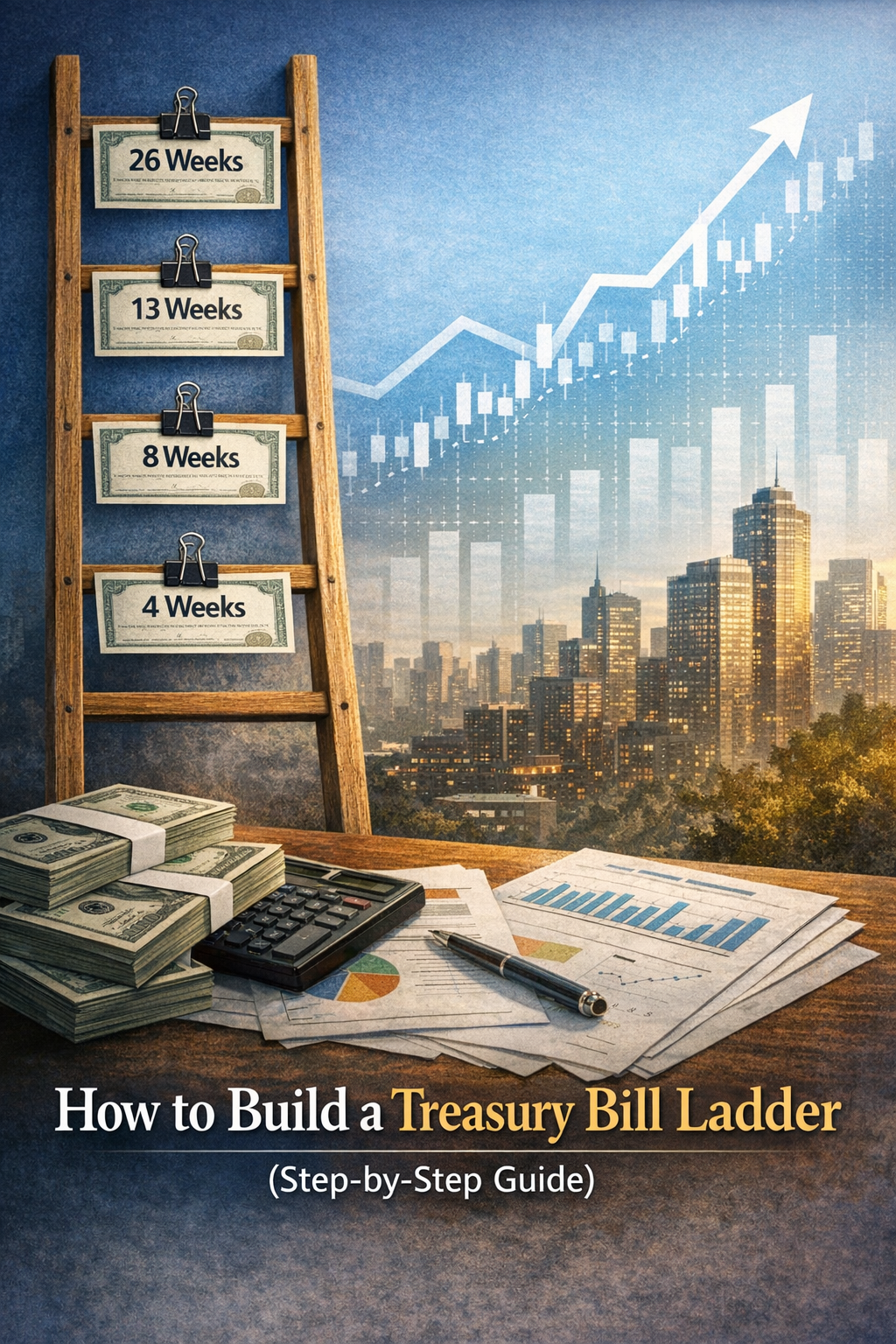

If you like the idea of T-bills but do not want all your money tied to one maturity date, a ladder may help.

A Treasury ladder spreads money across multiple maturities so part of your cash becomes available on a regular schedule.

That gives you more flexibility than putting everything into one bill.

👉 Learn more here:

How to Build a Treasury Ladder

Or try the tool directly:

Build a Treasury Ladder

A Practical Way to Decide

Ask yourself these questions:

- When will I need this money?

- How certain is that timeline?

- Do I value flexibility or predictability more for this portion of cash?

- Would state tax treatment make a difference?

- Am I trying to optimize immediate access, or organize money by purpose?

Then match the tool to the job.

That is the core decision rule.

Do not ask, “Which one is better?”

Ask, “What is this money for?”

Frequently Asked Questions

Are Treasury bills safer than savings accounts?

Both are generally considered very safe when used properly, but they are protected in different ways.

Treasury bills are backed by the U.S. government.

High-yield savings accounts are bank deposit accounts and may be protected by FDIC or NCUA insurance when held at an insured institution, subject to coverage limits.

The bigger practical difference is usually liquidity.

Savings accounts prioritize access, while Treasury bills prioritize a defined maturity date and predictable structure.

Can Treasury bills pay more than a high-yield savings account?

Sometimes yes, sometimes no.

The better comparison is often after-tax return and whether you can leave the money untouched until maturity.

Are Treasury bills good for an emergency fund?

They can be useful for part of an emergency fund, but most people still need a savings portion for immediate access.

A common approach is to keep immediate emergency cash in savings and use Treasury bills only for the portion of cash you are less likely to need right away.

What is the biggest advantage of a savings account?

Immediate or near-immediate liquidity.

Savings accounts are usually better when the timing of your cash need is uncertain.

What is the biggest advantage of a Treasury bill?

Predictable short-term return with a defined maturity date.

Treasury bills are usually better when the cash has a known timeline and you can wait until maturity.

Final Thought

Treasury bills and high-yield savings accounts are not direct competitors.

They are complementary tools.

A savings account is usually best for money that needs to stay flexible.

A Treasury bill is usually better for cash that has a known timeline and can be put to work more intentionally.

The more clearly you assign a job to each dollar, the easier this decision becomes.

That is what good cash management really is.

Not picking one product forever.

But choosing the right tool for the right purpose.

Next Step

Choose the next step based on what you are trying to decide.

If you want to compare T-Bills against savings

Use the comparison tool to see how Treasury yields stack up against high-yield savings rates.

If you want to check current Treasury yields

Start with the live rates page before deciding which maturity fits your cash timeline.

If you want to estimate a T-Bill return

Use the calculator to estimate potential return for a specific amount and maturity.

If you want recurring access to cash

Learn how a Treasury ladder can spread maturities over time.