T-Bill Rates Today: How to Read Current Treasury Bill Yields

Learn how to read current T-Bill rates, compare Treasury bill terms, understand Treasury yields, and use live Treasury data to estimate short-term returns.

When people search for T-Bill rates today, they are usually trying to answer a practical question:

What can my cash earn if I put it into a Treasury bill right now?

That question sounds simple, but the answer depends on several things:

- the Treasury bill term

- the current yield

- the issue date

- the maturity date

- how long your money will be tied up

- whether you are comparing T-Bills with savings accounts, CDs, money market funds, or other cash options

A 4-week T-Bill and a 26-week T-Bill may both be short-term Treasury securities, but they do not always offer the same yield or fit the same cash need.

That is why reading current Treasury bill rates is not just about finding the highest number.

It is about matching the right maturity to the right job.

Want to see current rates first?

Start with the live rates page to view current Treasury rates and compare Treasury bills by term.

What Are T-Bill Rates?

T-Bill rates are the yields associated with short-term U.S. Treasury bills.

A Treasury bill, often called a T-Bill, is a short-term security issued by the U.S. Treasury. Instead of paying interest every month, Treasury bills are typically sold at a discount and mature at full face value.

That means your return usually comes from the difference between:

- what you pay for the bill

- what you receive when it matures

For example, if a T-Bill matures at $10,000 and you buy it for less than $10,000, the difference is your earnings if you hold it to maturity.

The quoted rate or yield helps investors compare one Treasury bill with another.

But the quoted yield is only part of the decision.

You also need to understand the bill’s term, maturity date, and how it fits your cash timeline.

Why T-Bill Rates Matter

T-Bill rates matter because they influence how investors and savers think about short-term cash.

When T-Bill yields are attractive, investors may compare them against:

- high-yield savings accounts

- certificates of deposit

- money market funds

- short-term bond funds

- cash sitting idle in checking accounts

Treasury bills are often used for money that needs to remain relatively safe but does not need to be available immediately.

Examples include:

- tax reserves

- business cash reserves

- money set aside for a future purchase

- emergency fund layers

- home down payment cash

- tuition money

- short-term savings goals

- Treasury ladder strategies

The main point is this:

T-Bill rates help you decide whether a specific Treasury bill term is worth considering for cash you can leave untouched until maturity.

Common Treasury Bill Terms

Treasury bills are short-term securities.

Common T-Bill terms include:

| T-Bill Term | Approximate Time Horizon | Common Use |

|---|---|---|

| 4-week T-Bill | About 1 month | Very short-term cash |

| 8-week T-Bill | About 2 months | Cash needed soon but not immediately |

| 13-week T-Bill | About 3 months | Quarterly cash planning |

| 17-week T-Bill | About 4 months | Intermediate short-term cash |

| 26-week T-Bill | About 6 months | Cash with a half-year timeline |

| 52-week T-Bill | About 1 year | Longer short-term cash planning |

The best term is not always the one with the highest yield.

The best term is usually the one that matches when you expect to need the money.

Want to estimate a specific term?

Use the calculator to estimate potential returns for available 4-week, 8-week, 13-week, 26-week, or 52-week Treasury bills when those terms appear in the live data.

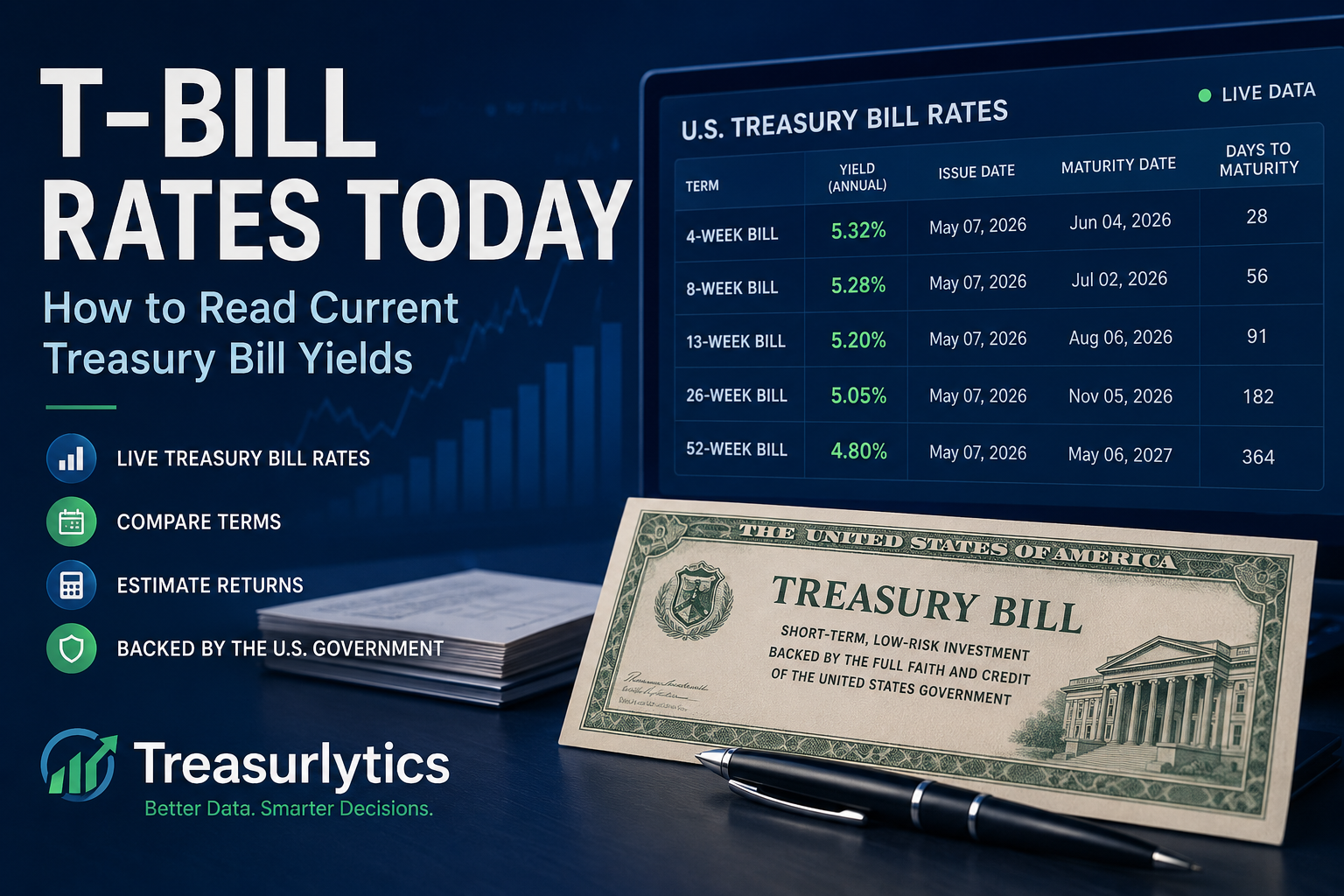

How to Read Current T-Bill Rates

When looking at current T-Bill rates, pay attention to more than the yield.

A good Treasury bill rates table should help you compare several fields.

1. Term

The term tells you approximately how long the bill runs before maturity.

A shorter term gives you cash back sooner.

A longer term may let you lock in a rate for more time.

For example:

- a 4-week bill may fit cash you need soon

- a 13-week bill may fit quarterly planning

- a 26-week bill may fit money you can leave alone for about six months

2. Yield

The yield is the annualized return indicator.

It helps you compare different T-Bills, even when they have different maturities.

However, an annualized yield does not mean you earn that full percentage over a few weeks.

A 4-week T-Bill with a quoted annualized yield does not pay a full year of interest. It earns a return for the shorter period it is held.

That is why a calculator can help translate the annualized yield into estimated dollars.

3. Issue Date

The issue date tells you when the Treasury bill starts.

This matters because the timing affects the actual holding period.

4. Maturity Date

The maturity date tells you when the bill is scheduled to pay its face value.

This is one of the most important fields for cash planning.

If you need money before the maturity date, the bill may not be the best fit unless you are comfortable selling early or using a brokerage market.

5. Days to Maturity

Days to maturity helps you compare terms more precisely.

For example, two bills may look similar, but one may mature sooner than the other.

6. Price per $100

Treasury bills are often priced relative to $100 of face value.

Because T-Bills are generally sold at a discount, the price per $100 can help show how much below face value the bill trades.

7. CUSIP

A CUSIP is an identifier for a specific security.

It helps distinguish one Treasury bill from another, especially when several bills have similar terms.

Example: Reading a T-Bill Rate

Suppose you are comparing a 13-week T-Bill and a 26-week T-Bill.

The 13-week bill gives you access to cash sooner.

The 26-week bill ties up cash longer.

If the 26-week bill has a higher yield, that does not automatically mean it is the better choice.

You still need to ask:

- Will I need this money before the 26-week maturity date?

- Am I comfortable locking in the rate for longer?

- Could rates change before I reinvest?

- Is the extra yield worth the reduced flexibility?

- Would a shorter T-Bill ladder make more sense?

A higher yield is useful only if the maturity also fits your cash needs.

T-Bill Rates Today vs Savings Account Rates

T-Bills and savings accounts are often compared because both are used for cash.

But they are not the same.

| Feature | Treasury Bills | High-Yield Savings Accounts |

|---|---|---|

| Return structure | Discount to face value | Interest/APY credited over time |

| Access to cash | Best if held to maturity | Usually immediate or near-immediate |

| Rate certainty | Known for that bill if held to maturity | Can change at any time |

| Term | Fixed maturity | No fixed maturity |

| State/local tax treatment | Generally exempt from state and local income tax | Usually taxable where applicable |

| Best use case | Planned cash with a known timeline | Emergency cash and daily liquidity |

A savings account is usually better for money you may need at any moment.

A T-Bill may be better for money with a specific timeline.

👉 Compare both side by side:

Compare T-Bills vs Savings

Why the Highest T-Bill Rate Is Not Always the Best Choice

Many people naturally look for the highest yield.

That is understandable.

But with Treasury bills, the highest yield is not always the best fit.

A T-Bill has a maturity date. If you choose a longer maturity only because the yield is slightly higher, you may create a cash-flow problem.

For example:

- You need the money in 6 weeks.

- A 26-week bill has a higher yield than a 4-week bill.

- You buy the 26-week bill.

- Then you need the cash before maturity.

That could create inconvenience or force you to sell early.

A better approach is to start with your timeline first.

Then compare rates among bills that fit that timeline.

How T-Bill Rates Affect Your Estimated Return

A T-Bill rate is useful, but most people ultimately want to know the dollar amount.

For example:

- If I invest $5,000, what might I earn?

- If I invest $10,000, what might I earn?

- If I choose a 4-week bill instead of a 26-week bill, how different is the estimate?

- How much will the bill be worth at maturity?

That is where a calculator helps.

A T-Bill calculator can estimate:

- investment amount

- annual yield

- days to maturity

- estimated interest

- purchase price

- maturity value

- annualized return

Estimate your own Treasury bill return

Choose a live Treasury bill, enter an investment amount, and estimate the potential return by maturity.

How Often Do T-Bill Rates Change?

T-Bill rates can change as market conditions change.

Several factors can influence Treasury bill yields:

- Federal Reserve policy expectations

- inflation expectations

- demand for safe assets

- Treasury auction results

- short-term funding conditions

- investor demand for liquidity

- broader economic uncertainty

Because rates can move, it helps to check current data before making a cash decision.

A rate you saw last month may not be the same rate available today.

That is why Treasurlytics focuses on tools that connect rates, calculators, comparisons, and ladder planning.

What Does “Live T-Bill Data” Mean?

When a page says it uses live T-Bill data, it should mean the tool is loading currently available Treasury bill information instead of relying only on a static example.

Useful live data fields may include:

- current available bill terms

- annualized yields

- issue dates

- maturity dates

- days to maturity

- CUSIPs

- price per $100

- auction or market-related fields when available

Live data does not mean rates change every second like a stock quote.

It means the page is designed to pull current Treasury data from its connected data source so that visitors can work with recent available information.

👉 See current available Treasury data here:

View Live Treasury Rates

How to Use Current T-Bill Rates for Cash Planning

A practical way to use T-Bill rates is to start with your goal.

If you need cash soon

Look at shorter T-Bills first.

For example:

- 4-week T-Bills

- 8-week T-Bills

- 13-week T-Bills

These may be more useful when your cash timeline is measured in weeks or a few months.

If you can wait longer

Look at longer T-Bill terms.

For example:

- 17-week T-Bills

- 26-week T-Bills

- 52-week T-Bills

These may make sense when you can leave the money invested until maturity.

If you want repeated access to cash

Consider a ladder.

A Treasury ladder spreads cash across multiple maturities so that some money becomes available at regular intervals.

This can reduce the problem of putting all your cash into one maturity date.

👉 Learn how this works:

How to Build a Treasury Ladder

Build a Treasury Ladder

T-Bill Rates and Treasury Ladders

T-Bill rates are especially useful when building a ladder.

A ladder might use several bill terms so that cash matures in stages.

For example, instead of putting all your cash into one 26-week bill, you might spread it across several maturities.

The goal is to balance:

- yield

- liquidity

- flexibility

- reinvestment timing

When current T-Bill rates are attractive, a ladder may help you earn on cash while avoiding the risk of locking everything into one date.

The exact ladder structure depends on your cash needs.

Questions to Ask Before Choosing a T-Bill

Before choosing a Treasury bill based on today’s rate, ask:

- When will I need this money?

- Do I need immediate access?

- Can I hold the bill until maturity?

- Is the extra yield worth a longer maturity?

- Am I comparing after-tax returns?

- Would a ladder be more flexible than one bill?

- Am I using this for cash preservation or long-term growth?

- What happens when the bill matures?

T-Bills can be useful, but they work best when they have a clear purpose.

Common Mistakes When Reading T-Bill Rates

Mistake 1: Choosing only the highest yield

The highest yield may come with a maturity that does not fit your timeline.

Mistake 2: Ignoring liquidity

If you need cash before maturity, a savings account may be more practical.

Mistake 3: Confusing annualized yield with actual short-term return

A short-term T-Bill does not earn a full year of interest. The yield is annualized for comparison.

Mistake 4: Forgetting taxes

Treasury securities are generally exempt from state and local income tax, but federal tax still matters.

Mistake 5: Not planning reinvestment

When a T-Bill matures, you need to decide what happens next.

If rates have changed, your next bill may offer a different yield.

How Treasurlytics Helps You Read T-Bill Rates

Treasurlytics is designed to connect the pieces of short-term Treasury decision-making.

You can:

- view current Treasury rates

- filter rates by bill, note, or bond

- compare Treasury terms

- estimate T-Bill returns

- compare T-Bills against savings accounts

- build a Treasury ladder

- read educational guides before deciding

Start here:

Then estimate a return:

Then compare alternatives:

Frequently Asked Questions

What are T-Bill rates today?

T-Bill rates today are the current yields available on Treasury bills based on recent Treasury data and market conditions.

Because rates can change, it is useful to check live Treasury rates before estimating a return or choosing a maturity.

Where can I find current Treasury bill rates?

You can view current Treasury bill rates on the Treasurlytics live rates page.

The rates table lets you compare Treasury bills by term, yield, issue date, maturity date, days to maturity, CUSIP, and price-related fields.

How do I calculate a T-Bill return?

To estimate a T-Bill return, you need the investment amount, yield, and days to maturity.

A calculator can use those inputs to estimate interest earned, purchase price, maturity value, and annualized return.

Is a 4-week T-Bill better than a 26-week T-Bill?

Not automatically.

A 4-week T-Bill gives you cash back sooner, while a 26-week T-Bill keeps money invested longer.

The better choice depends on your timeline, liquidity needs, and the current yield difference.

Are T-Bill rates the same as savings account rates?

No.

Savings accounts usually quote an APY and offer ongoing access to cash.

T-Bills have fixed maturities and are typically purchased at a discount to face value.

Both can be used for cash management, but they work differently.

Do T-Bill rates change every day?

T-Bill yields can change as market conditions, Treasury auctions, and investor demand change.

That is why it helps to check current Treasury data before making a decision.

What is the best T-Bill term?

The best T-Bill term is the one that matches your cash timeline.

If you need the money soon, a shorter bill may be more appropriate.

If you can leave the money invested longer, a longer bill may be worth comparing.

Can I use T-Bills for an emergency fund?

T-Bills can be useful for part of an emergency fund, but they are usually not ideal for all emergency cash.

Many people prefer to keep immediate emergency money in a savings account and use T-Bills for cash they are less likely to need right away.

Final Thought

T-Bill rates are useful because they turn short-term cash into a decision.

They help you answer:

- What can this money earn?

- How long will it be tied up?

- When will it mature?

- Is the return worth the wait?

- Would a different term fit better?

- Should I compare it with savings or build a ladder?

The goal is not to chase the highest number on the page.

The goal is to match your cash with the right maturity.

A Treasury bill can be a powerful cash management tool when the timeline is clear.

Current T-Bill rates simply help you make that decision with better information.

Next Step

Choose the next step based on what you are trying to do.

If you want to check current T-Bill yields

Start with the live rates page to see current Treasury bill rates and compare terms.

If you want to estimate a T-Bill return

Use the calculator to estimate potential return for a specific investment amount and maturity.

If you want to compare T-Bills with savings

Compare Treasury bills against high-yield savings accounts using practical cash-management tradeoffs.

If you want recurring access to cash

Learn how a Treasury ladder can spread maturities over time.

How to Build a Treasury Ladder

Build a Treasury Ladder

If you want to understand Treasury bills first

Read the beginner guide to Treasury bills.

If you want the broader Treasury picture

Learn how Treasury bills fit into the larger family of U.S. Treasury securities.